As a very wise person once quipped:

Homeowners Live in the Monthly Payment, Not the Purchase Price.

Mortgage interest rates are understandably a major consideration when purchasing a home, especially after the dramatic increases we have seen since 2022. Higher rates translate directly into higher monthly mortgage payments, which means purchasing power has declined for many buyers. Add to that the recent week-to-week volatility in rates, and it becomes even harder for buyers to anticipate monthly payments and maintain comfortable debt-to-income ratios.

At The Excelsior Team at Brown Harris Stevens, we believe knowledge is power. Understanding how interest rates affect your monthly mortgage payment allows you to better evaluate your budget, your timeline, and your true purchasing power. The goal is not to ignore rates, but to understand them in real dollar terms rather than abstract percentages.

Let’s break it down.

Why Monthly Payments Matter More Than Price

Homeowners live in their monthly payments, not the purchase price. That is the number that determines comfort, flexibility, and long-term sustainability.

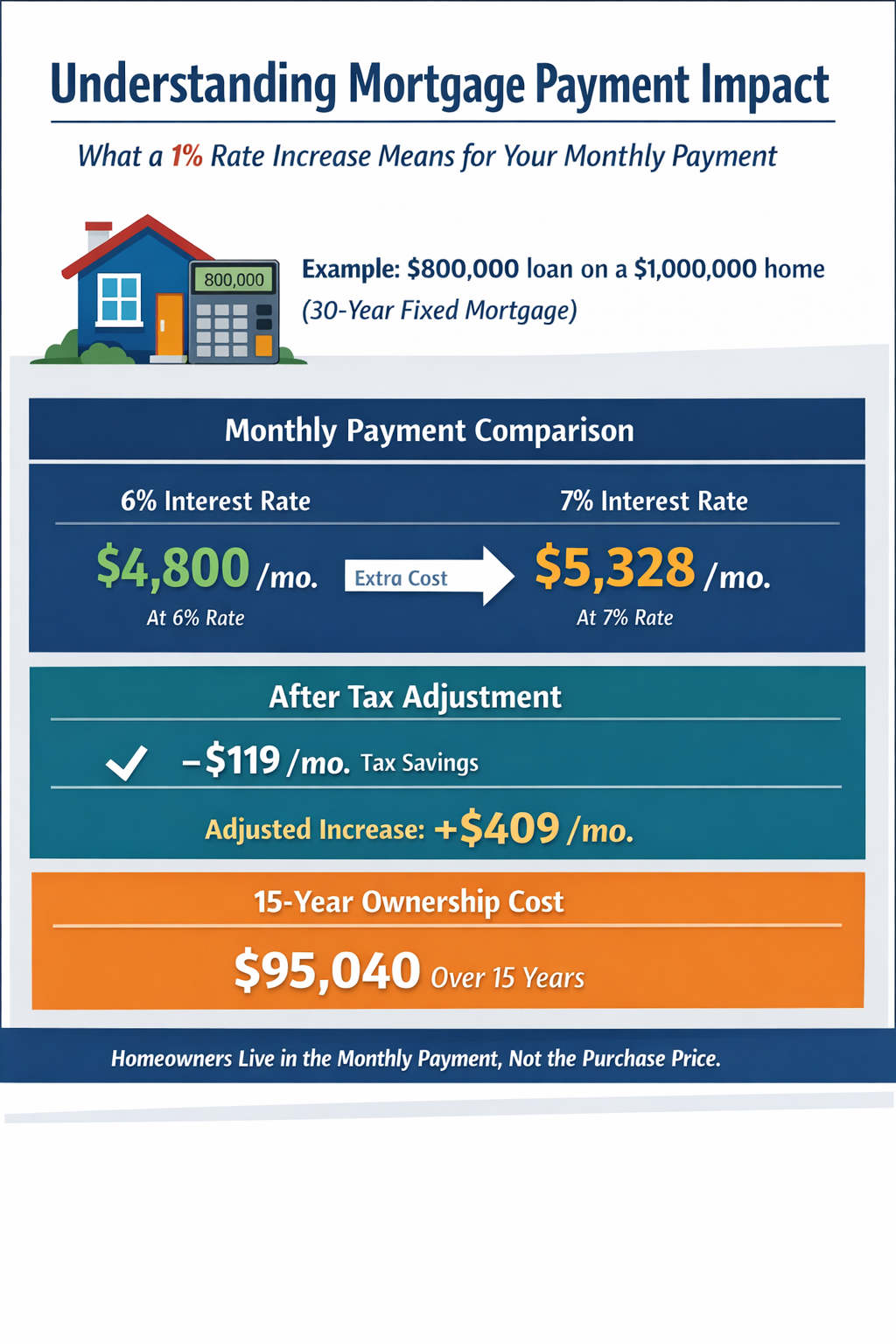

To illustrate this, we will compare two interest rates on a conventional 30-year fixed-rate mortgage: 6 percent and 7 percent. That one percent difference, often referred to as 100 basis points, represents the approximate swing between more favorable rates and the high-water mark seen in late 2024.

Rather than thinking in decimals, the most useful way to evaluate this change is in dollars.

The Math Behind a Mortgage Payment (Without the Pain)

For the mathematically inclined, the formula for calculating a monthly mortgage payment looks like this:

M = L[c(1 + c)^n] / [(1 + c)^n – 1]

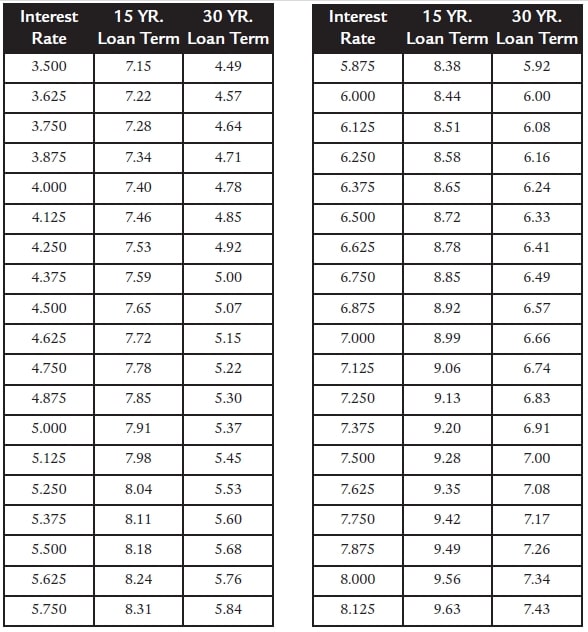

If that equation brings back unpleasant memories of high school math, you are not alone. Fortunately, there is a much simpler tool that does most of the heavy lifting: the mortgage amortization factor chart.

This chart shows the monthly principal and interest payment per $1,000 borrowed, based on interest rate and loan term. The vertical column lists interest rates, and the horizontal row lists loan terms. Find your rate, move across to the 30-year term, and you have your factor.

For example:

- A 30-year mortgage at 6% has an amortization factor of 6.00

- At 7%, the factor is 6.66

This does not mean the factor always mirrors the rate. It is simply a convenient coincidence at 6%, and an easy reference point to remember.

Turning the Factor Into Real Dollars

The amortization factor tells us that for every $1,000 borrowed at 6%, the monthly payment is $6.00.

Since most of us are not buying homes in $1,000 increments, it is far more useful to think in $100,000 increments. To do that, simply move the decimal point two places.

- At 6%, each $100,000 borrowed costs $600 per month

- At 7%, each $100,000 borrowed costs $666 per month

The difference between those two numbers is $66 per $100,000 borrowed.

What a 1% Rate Increase Really Costs

Let’s apply this to a real-world scenario.

Assume you are purchasing a $1,000,000 apartment and financing 80% of the purchase price, or $800,000.

- The monthly difference between a 6% and 7% rate is:

- $66 x 8 = $528 per month

That is not insignificant. On an annual basis, it equals $6,336. But context matters.

At a 6% rate, the monthly principal and interest payment on an $800,000 mortgage is $4,800. Add a reasonable $2,000 monthly maintenance payment, and the total monthly carrying cost is $6,800 before taxes.

In that context, a $528 increase represents an 8.33% increase in total monthly carrying costs, not as significant a spike as you might think.

The Tax Deduction Factor

One of the key advantages of ownership versus renting is the tax deductibility of mortgage interest. While the balance between principal and interest shifts over time, the early years of a mortgage are heavily interest-weighted. For many buyers, approximately 75% of the payment is interest during the initial years.

Let’s revisit the $528 monthly increase.

- Annual increase: $528 x 12 = $6,336

- Interest portion assumed deductible: 75%

- Deductible amount: $4,752

Assuming a 30% tax bracket, the annual tax savings would be approximately $1,426, or about $119 per month.

That reduces the effective monthly increase from $528 to roughly $409.

Ownership Horizon Matter

How long you plan to own the apartment should play a major role in your decision.

Let’s take a conservative 15-year ownership horizon.

- Monthly cost of higher rate: $528

- Annual cost: $6,336

- 15-year cost: $95,040

That figure represents less than 1 percent of the total purchase price of the apartment and does not account for potential appreciation over that time period.

Putting Rates in Perspective

We do not buy or live in a vacuum. In New York City, unless you benefit from rent control or family-owned housing, your choice is typically between renting and owning.

While rates are higher than they were a few years ago, they remain historically moderate. For buyers who:

- Have the necessary down payment and post-closing reserves

- Can navigate the purchase process without undue time pressure

- Plan to hold the property for more than a few years

…the rent-versus-buy equation often still favors ownership.

Final Thought

Whatever decision you make in response to higher interest rates, make it with a clear understanding of what those rates mean in dollars, not decimals.

Doing so allows you to assess trade-offs rationally, maintain perspective, and avoid letting short-term fear override long-term financial logic.

And remember, homeowners live in the monthly payment, not the purchase price.